Sticking to our proven Investment Philosophy : ‘Never Fully Invest at All Times’

Pheim Unit Trusts Berhad (PUTB) started its operation in April 2001, among the first funds introduced to retail investors was its flagship Islamic Balanced Fund – Dana Makmur Pheim. Just like any other Unit Trust Schemes (UTS) in moderate risk category, Dana Makmur Pheim provides an ideal avenue for small investors (and high-net-worth investors) to gain exposure to a wide range of investment opportunities at a reasonable cost. Investment through UTS is one of the best medium to long-term investment decisions that smaller investors can make with a view to accumulating capital and beating inflation over the long run.

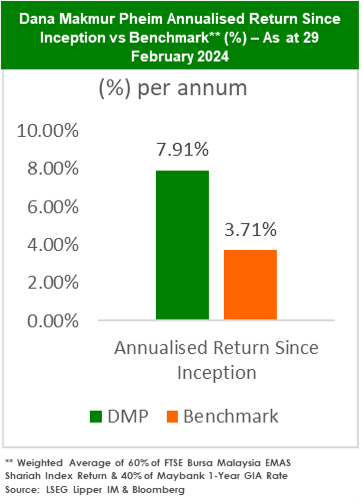

Dana Makmur Pheim was established on 28 January 2002, and generated a Cumulative Return of +435.80%, which is equivalent to an Annualised Return Since Inception of +7.91% per annum, as at 29 Feb 2024. Cumulatively, the Fund outperformed its benchmark return by a huge margin of 312.69%.

Over the past 22 years since inception, the Fund has established a good long-term performance track record. At its best, Dana Makmur Phiem was ranked No.1 for 11 consecutive years by LSEG Lipper (a provider of global fund performance data) in terms of total return under the Islamic Mixed Asset MYR Balanced – Malaysia category for the 10-year period ended 31 December 2022.

Dana Makmur Pheim (DMP) has won a total of 56 LSEG Lipper Fund Awards, consisting of 35 Malaysia Islamic Awards and 21 Global Islamic Awards. Not a single fund in this category has ever won so many awards in Malaysia’s unit trust history.

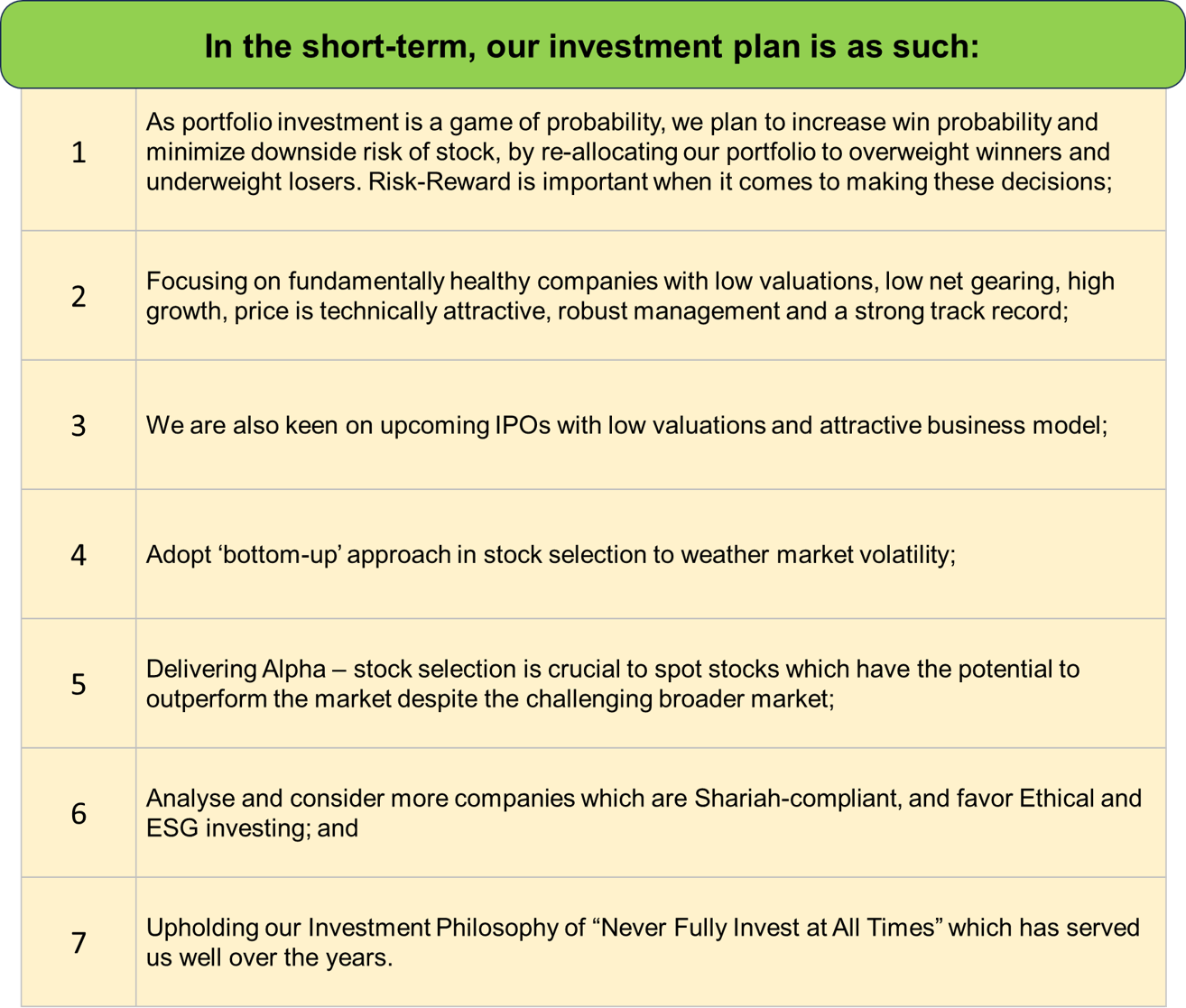

According to the Pheim Asset Management Sdn Bhd, our external investment manager of the Fund, the fund’s consistency and long-term track record comes from the bottom-up selection of stocks based on detailed fundamental analysis.

The analysis and investment decision-making process involves fundamental screening, talking to the companies’ management and determining the valuation with Pheim’s Investment Criteria. Pheim Asset Management Sdn Bhd maintains its investment strategy of ‘bottom-up’ approach in stock selection with the aim of alpha play to outperform the benchmark index. It aims for value stocks that are fundamentally sound, i.e. low net gearing, attractive valuation, good corporate governance coupled with strong future earnings growth.

Furthermore, the Fund also positioned itself well with stock exposures in Property, Construction and Oil & Gas sectors. The Fund exercises its selling discipline well, by locking in profit for those making handsome returns to our portfolio and stocks deemed overvalued amid current market volatility.

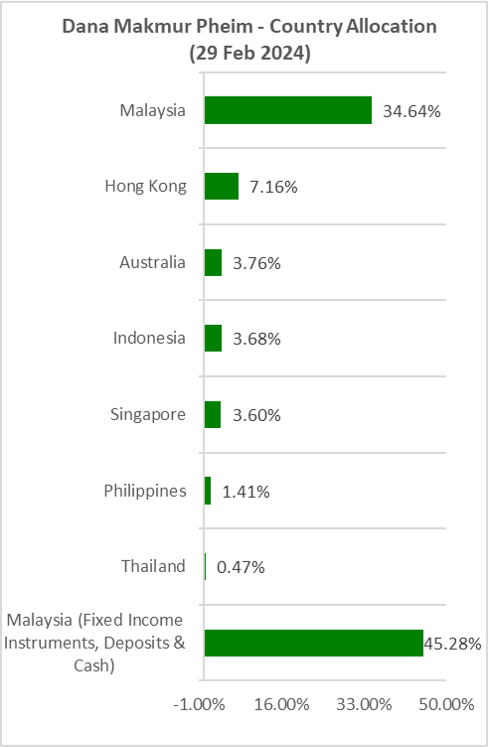

The Fund has an annual management fee of up to 1.5% p.a. and an annual trustee fee of 0.055% p.a.. The minimum initial investment amount is RM1,000 and the minimum additional investment amount is RM100. It is also a Shariah-compliant fund that invests in Shariah-compliant equities listed on Asia Pacific ex-Japan markets. Other than returns, investors of the Fund enjoy the benefit of country diversification, as it allocates its money in more than seven Asian countries.

Recently Dana Makmur Pheim has been experiencing stagnant NAV growth, what are the main causes?

DMP has delivered a return of -0.67% year-to-date (as of end-Feb 24) mainly dragged down by the local sukuk and equity.

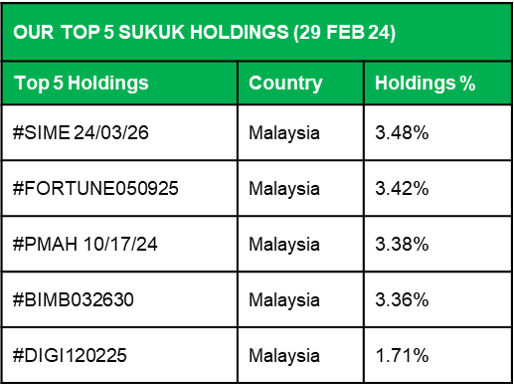

Local Sukuk and Islamic Liquid Assets

Prices of the sukuk have come down for the past 2 years amid the rising interest rate atmosphere, hence impacting the portfolio NAV. With regards to that, we have already taken steps to reduce our sukuk exposure from 30.78% (Feb 2023) to 24.08% (Feb 2024). The liquidated sukuk are promptly placed into short-term Islamic money market funds which have a rate of 2.90% p.a. – 3.90% p.a. (over various placement durations spanning from 1 day to over 3 months).

Having said that, the sukuk that were purchased for DMP are mostly short-term sukuk (of which the maturity dates average around 2 years and 9 months from 31 Dec 2023) and we intend to adopt a ‘buy-and-hold’ (i.e. hold till maturity) investment strategy for our sukuk and we do not realise any actual losses on it, though in the short-term DMP will exhibit a paper loss due to the low valuation of these sukuk (mark to market). In the meantime, DMP would enjoy the benefit of consistently receiving coupon payments which range from (at a coupon rate ranging between 3.75% p.a. – 5.65% p.a.) from the credit issuers.

Overall, in terms of the long-term plan for our Islamic fixed income strategy, DMP will weather through the adverse sukuk market by taking sukuk which have a short maturity time of 3 years and below as well as closely monitoring and making placements in selected Islamic money market funds in the hope to reposition DMP back into long-term sukuk once we determine that macro factors and lower interest rate will once again favour long-term sukuk investors.

Meanwhile, on the equity side, our portfolio is affected by the slowdown of China’s economy and massive outflow of foreign funds from the nation which dragged down the performances in our China stocks and certain mining/energy stocks in Malaysia, Australia and Singapore (China being the largest major consumer for hard commodities in the world).

Some insights

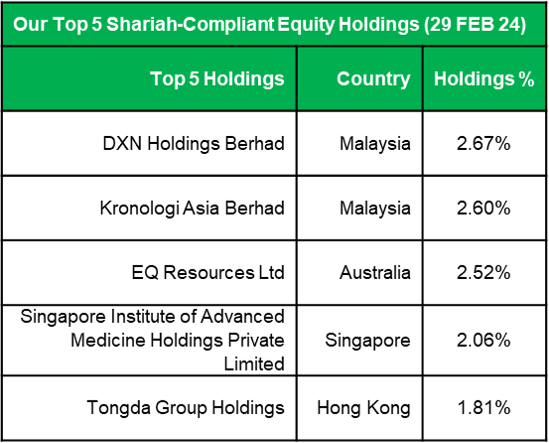

EQ Resources Limited (EQR) is an Australia-based tungsten mining company. The Company is focused on expanding its tungsten assets at Mt Carbine in North Queensland (Australia) and at Barrueco Pardo in the Salamanca Province (Spain). It also holds gold exploration licenses in New South Wales, at Panama Hat (Broken Hill) and Crow Mountain. The project is on granted mining leases with power, water, tailings storage and environmental approvals in place for tungsten production and quarrying.

Despite recently falling out of favour of speculators, we believe that there is much potential for upward growth for EQR in the long term as the US-China trade wars have caused the US to begin exploring other means to source valuable commodities and metals. Tungsten is a metal with a wide range of uses, the largest of which is as tungsten carbide in cemented carbides.

(Source: U.S. Geological Survey, Mineral Commodity Summaries, January 2024)

An estimated 60% of the tungsten consumed in the United States was used in cemented carbide parts for cutting and wear-resistant applications, primarily in the construction, metalworking, mining, and oil- and gas-drilling industries. Cemented carbides (also called hard metals) are wear-resistant materials used by the metalworking, mining, and construction industries. (Source: U.S. Geological Survey, Mineral Commodity Summaries, January 2024). Potential substitutes for cemented tungsten carbides include cemented carbides based on molybdenum carbide, niobium carbide, or titanium carbide; ceramics; ceramic-metallic composites (cermets); and tool steels. In some applications, substitution would result in increased cost or a loss in product performance.

The US’s annual consumption of the metal sat at around 11,400 tonnes in 2021 (Source: US Geological Survey (“USGS”), 2021), according to the US Geological Survey (“USGS”), and this figure is growing. At the same time, however, domestic primary production currently sits at zero. Tungsten Mining and Production companies like EQR will benefit from the escalation of the geo-political tensions between US and China in this manner and as the demand for this already scare mineral would be multiplied.

DXN Holdings is primarily involved in the sale of health oriented and wellness consumer products consisting of fortified food and beverages (FFB), health and dietary supplements (HDS), personal care and cosmetics (PCC) and other products. It has established a global market presence in 180 countries. Although DXN’s share price remains below its IPO price, the Company commits to pay dividend every quarter, rendering dividend yield of over 4% and currently trading at undemanding valuation of below forward PE of 10x. with solid balance sheet of net cash position as of to date. The Group commences operation in Brazil by Mar 24 and it could further expand its footprint in Latin America.

For Kronologi, we remain optimistic on the Group’s business outlook as recovery in China economy could lift its earnings outlook for cloud business there. China market now contributed 27.7% of group revenue for FY2023, ahead of the Philippines (24.2%), and behind Singapore (34%). We like the stock for its market leading position in the Enterprise Data Management industry. Krono’s business will benefit from rapid growth of unstructured data, demand growth of data digitalisation, expansion of data centres, and growing demand of cloud services.

Tongda Group specialises in global smart mobile communications and consumer electronics products, covering handsets, smart home appliances, automotive, household and sports goods, network communications facilities and 5G related business. Recently, Tongda has announced plans to dispose its Apple business and purchase back smart electrical appliances and motor businesses, in order to mitigate geopolitical risks and boost capital for future new business development. This will allow Tongda to focus more on non-Apple customers’ market share gains and boost capital for new businesses given the likely smartphone recovery in 2024, while business buyback should accelerate profitability improvement driven by order wins in FY24-25E. The disposal to drive smartphone casing growth as Tongda can focus more on non-Apple customers such as Honor, Xiaomi, Vivo and Transsion with share gains and an improving UTR amid smartphone market recovery in 2024.

So, what is the fund manager’s market outlook for the year and how is it positioning the fund for another year of outperformance?

We reckon that US rate hike cycle is at the tail-end and any rate hike would be minimal moving forward. In fact, in December 2023, the US Federal Reserve released the updated Fed dot plot, which showed a projected 75 bps interest rate cut in 2024 from current fed funds target rate of 5.25%-5.50% as core PCE rose just 0.1% in November 23 and was up 3.2% from a year ago.

On the local front, we expect BNM to keep OPR unchanged at 3.00% for 2024 in the absence of demand-pulled pressures although monthly CPI is likely to trend higher depending on the pace of subsidy rationalisation. Also, fiscal consolidation helps limit debt issuances which further lend a support to the bond prices. The narrowing rate differential between the 10-year US Treasury (prevailing yield of 4.05%) and MGS (current yield of 3.90%) also bodes well to the foreign fund flows into local capital market.

We expect that the market will continue to exhibit volatility with few downside risks which could spook investor confidence, in the likes of geopolitical risks (i.e. lingering Ukraine-Russia war and Gaza crisis), potential economic slowdown in the US, China and EU coupled with resurgence of inflation pursuant to Red Sea disruptions.

Stock performances in HK/China look less promising as the whole macroeconomic picture of China still looks challenging, aggravated by the negative headlines of the Chinese real estate crisis and high youth unemployment rate.

Moving forward, we will re-strategize and reshuffle our portfolio towards more defensive and local stocks. This, of course, would temporarily impact the DMP’s distribution to the unitholders. However, the strategy could uplift the performance of the fund in the medium to longer-term and deliver consistent distribution to the long-term unitholders. Hence, it is advisable for long-term investors to stay invested during the current market conditions, and implement dollar-cost averaging to diversify your investment risk and grow your wealth in the long-run.

Disclaimer

While the following informational materials contained within are believed to be reliable and gathered from credible sources, there is no warranty or guarantee of the accuracy of the information provided by the company and its group affiliates, employees or directors. The material provided is for information purposes only and of itself does not constitute nor should be construed as an offer or solicitation for purchase or investment into any financial instrument or security.

The above information has not been reviewed by the Securities Commission and is subject to relevant warning, disclaimer, qualification or terms and conditions stated herein. The material should not be construed as formal investment, legal, tax or accounting advice and such formal advice should be acquired by any individual investor prior to making an investment.

The strategies, instruments and/or opinions in that regard contained within the material may not be suitable or appropriate for all investors. The material does not account for the individual investor’s risk requirements, needs, circumstances and objectives. The information contained herein does not have any regard to the specific investment objectives, financial situation or particular needs of any person. Views, thoughts and opinions expressed herein belong solely to the author and not necessarily to the author’s employer. We assume no responsibility or liability for any errors or omissions in the content of this presentation slides. Investors may wish to seek advice from a financial advisor before making any investment decision. Investors should not be solely relied on ratings or rankings provided to make an investment decision. An investment is subject to investment risks, including the possible loss of the principal amount invested. Past performance is not indicative or a warranty of future results.