Market Review April 2026

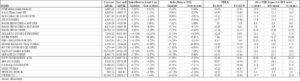

Risk assets corrected sharply amid escalating Middle East war when the US and Israel launched unilateral pre-emptive strikes on Iran on February 28. In retaliation, Iran closed the Strait of Hormuz through which about 20% of crude oil and LNG exports from the Gulf pass through, resulting in higher energy prices across the globe. Treasury yields moved materially higher. Key stable macro variables face challenging headwind as market expectation on inflation rate is likely to move higher. The magnitude and severity of the impact on inflation and the world economic growth will rest upon the duration of the US/Israel and Iran war. The World Index declined 6.55% in March. The MSCI Far East Ex. Japan index underperformed, declining 13.69%, driven by North Asia markets, in particular Korea and Taiwan markets which are more dependent on energy imports from the Middle East. Within the Asia region, ASEAN equities declined 7.38%, led by Indonesia (-14.42%) and Vietnam (-10.95%) markets. Regional currencies weakened against the USD. The best performing currencies were Hong Kong dollar (-0.20%) and Chinese Yuan (-0.47%), while the weaker ones were Philippines Peso (-5.07%) and Korean Won (-5.03%).

US indices corrected across the board on risk aversion due to heightened geopolitical tension in the Middle East. For the month, Dow Jones Industrial Average (DJIA), S&P 500 Index and Nasdaq Composite declined 5.38%, 5.09% and 4.75% respectively. The US economy slowed as the first revision of the 4Q GDP reading was lower than the previous quarter estimate and well below the Dow Jones consensus forecast of 1.5% growth rate. It is also a considerable slowdown from the 4.4% gain in the prior period, hampered by a record long government shutdown that saw the government spending tumbled 16.7%. Although the US is a net exporter of crude oil, it is nevertheless facing substantial price increases in gasoline and oil products due to global price shocks and supply chain disruptions. Given the prevailing market situation, the Fed is expected to be reluctant to shift any time soon. The IMF sees little room for the Fed to cut interest rates in 2026.

The Stoxx Europe 600 Index corrected 8.00% from the prior month as energy price surged and inflation climbed to 2.5% in March from 1.9% in February, exceeding the European Central Bank (ECB)’s 2% target. The ECB held the interest rate at 2% in March, maintaining a cautious stance on elevated inflation risks. The unemployment rate in the Euro Area edged up to 6.20% in February 2026, rising from 6.10% in January. The energy and defensive sectors performed relatively better.

Hong Kong and H shares indices continued to soften. Hang Seng Index and Hang Seng China Enterprises Index declined 6.92% and 5.48% respectively as concerns over slower China economic growth and geopolitical risks weighed on investors’ risk appetite. During China’s Two Sessions meeting in March, the Government Work Report sets key economic and social goals, lowering the growth target from 5% in 2025 to 4.5%-5% in 2026. The adjustment aims to allow 2026 economic policies to focus more on improving growth quality while creating room for structural adjustments, reforms, and risk prevention.

South Korea’s KOSPI Index corrected sharply, declining 19.08% in March driven by negative news flow in memory sector and geo-political development in the Middle East, as well as profit taking after the sharp 48.28% run in the first two months of the year. There were concerns over future memory demand due to Google’s newly introduced TurboQuant technology that can reduce memory usage per task by up to six times. Economic activities remained robust. Korea’s industrial output posted its fastest growth in five years and eight months in February, mainly driven by gains in semiconductor production. The semiconductor production surged 28.2% from a month earlier, on the back of growing global demand driven by the artificial intelligence (AI) boom.

Taiwan’s TWSE Index declined, dropping 10.42% on profit taking. The market had risen 22.98% in the first two months of the year. Economic indicators remained healthy. Taiwan’s economic monitoring indicator flashed a red light for the third straight month in February, with the composite score rising to its highest level in more than four years according to the National Development Council (NDC). The composite index climbed one point from a month earlier to 40, the highest since July 2021, remaining in the red zone that signals an overheating economy.

Singapore’s STI corrected by 2.19% in March on global risk-off sentiment. Economic activities remained resilient. The S&P Global Singapore PMI jumped to 59.2 in February 2026 from 56.8 in January, marking the thirteenth consecutive month of expansion and the second-fastest pace on record. New orders rose at the quickest rate in 18 months, supported by stronger domestic and external demand, while output expanded historically fast, led by transport, information and communication.

Malaysia’s KLCI declined 1.53% on profit taking. Bank Negara Malaysia, somewhat surprisingly, expects economic growth of between 4%-5% this year, revising its forecast slightly upwards from 4%-4.5%, supported by strong household spending. Inflation was expected to remain moderate in 2026, in part due to policies aimed at cushioning the impact of rising commodity and energy prices

Thailand’s SET Index declined 5.24% in March on profit taking after registering strong gain year to date. Thailand’s consumer confidence index rose to 53.7 in February 2026 from 52.8 in January, marking the highest level since last May. The improvement was supported by the central bank’s rate cut to 1% and expectations that the new government after last month’s elections would introduce economic measures, including policies to provide cushion from high energy prices, promote household consumption, boost tourism and promote trade and investment incentives and farming support.

Jakarta Composite Index declined 14.42% on continued outflow by foreign investors. Indonesia retail sales accelerated to 6.9% YoY in February (from 5.7% in January), driven by food & beverages and household equipment spending, with the Ramadan season lifting monthly growth to +4.4% MoM. However, Consumer Confident Index softened to 125.2 (from 127 in January), reflecting weaker sentiment among lower- and upper-income households on income and job prospects, while middle-income confidence edged up on improved job outlook.

The Philippines PSE Index declined 10.02%. The S&P Global Philippines Manufacturing PMI rose to 54.6 in February 2026 from 52.9 in January, reflecting stronger manufacturing activity supported by sustained growth in new orders and the fastest pace of output expansion since November 2018. Inflation edged higher to 2.4% YoY in February 2026 from 2.0% in January, in line with market expectations and remaining within the central bank’s target range.

Vietnam’s VN-Index declined 10.95%. Foreign investors were net sellers throughout the month. Domestically, tightening systemic liquidity is a growing concern; with several commercial banks now pushing 12-month deposit rates above 9%.

The shift to a dovish monetary stance in the US at the start of 2026 appears now to have been upended by the war in the Middle East. After an almost 12 months of twist and turns in the US tariff saga, the market is still divided on impact of higher tariffs on macro variables such as inflation and economic activities. Meanwhile, US corporate earnings, especially in the technology sector, continue to be key pillar to hold up risk assets. US market valuations are at historical high, and the high valuation is further driven by strong capital expenditure drive for AI, which has raised questions as to whether the humongous expenditures in AI will generate the anticipated returns. The semiconductor and AI investment cycle may move into a more difficult phase as investors will start to be more discerning with regard to their return on investment. The supply and demand dynamic in the semiconductor cycle, on the margin, with supply capacity gradually improving at a time when global demand soften on lower GDP growth outlook, can potentially result in headwinds for the industry.

Geo-political developments as well as policy directions in the major economies, in particular US and in China, remain on our radar screen. The market is still watchful of developments in Trump’s tariffs for the key trade partners. Following the US Supreme Court’s recent ruling that the Trump Administration’s reciprocal tariffs are illegal, and the subsequent announcement by Trump to impose a new 15% tariffs on imports, uncertainties remained. The market is also attentive to other US policy pronouncements that would have major fiscal, financial and economic implications. Investors, by and large, appear to be comfortable with Trump’s “Big Beautiful Bill” that has been signed into law, notwithstanding that it will substantially increase US federal deficit and government debt. Meanwhile, new geo-political fissures have opened up with the recent US military raid and capture of Venezuela President, Nicolas Maduro Moros, and the repeated utterings by President Trump of his intention to bring Greenland within the US fold, militarily if necessary. Adding to these is the flare up of the military conflict between the US/Israel and Iran that has engulfed the entire Middle East and choked the supply of crude oil and LNG from the region to the world. These developments further hightened tension in global geo-politics. In the near term, the US mid term election to be held in the later part of 2026 may change the balance of power in the US Congress, and have significant impact on US policies in the remaining years of Trump’s term. These developments will create uncertainities for investors. The duration of the Middle East war has added to uncertainty in global growth outlook as supply chain disruptions in energy sources among other things push inflation higher and change macro variables assumption.

In Asia, the focus is on the pace of China’s economic recovery which has been weaker than expected. The tariff issues with the US and continuing efforts to broaden restrictions on sales of tech equipment and services to Chinese entities can only exacerbate the economic situation in China. The Chinese property sector continues to face challenges, and any sign of stabilization and growth will have positive catalyst for China’s economy and risk assets. The Chinese government continues to bring forth measures to help the economy. The Chinese government remains constructive on policies to spur economic activities to achieve economic growth target. The various measures have boosted market sentiments. However, the longer- term effectiveness on China’s economy continues to be closely watched. It may take time for the initiatives to bear fruits. The focus will be on addressing the challenges in the property market, lifting consumer sentiments and consumption, and countering the effects of the new US tariffs.

On external trade, countries with high export dependency for growth in the Asia region including ASEAN will face significant challenges arising from the US tariff policies. The disruption in supply chain realignment may result in temporary mismatch in corporate earnings delivery against market expectation during the initial stage of tariff implementation. To-date, while ASEAN countries’ exports to the US have been impacted by the tariffs, these countries have been able to mitigate the impact on the economic growth through trade diversifications. Many of these countries have now to also contend with having to manage disruptions in energy supplies and the ensuing price escalations.

While interest rates have started to be eased, there remains headwind for risk assets, including the impact of the still high interest rate on business and economic activities, uncertainties in US policies, the historically high market valuations in the US, the geo-political tension in various parts of the World and resulting disruptions to energy supplies, as well as the still slower than expected economic growth in China. However, in the investment space we are in, we believe there is room for cautious optimism. After years of prolonged sell down, and despite the upticks in recent months, China equities remain under-owned and their favourable valuation offer potential upside, particularly following the recent rounds of significant policy change initiatives from China.

We continue to apply our strategy of focusing on identifying fundamentally healthy companies with low valuations, low leverage, high growth, robust management and a strong track record, and adherence to our investment philosophy of “Never Fully Invest at All Times” which has served us well over the years.

We thank you once again for your continued faith in us, and hope to remain good stewards in our endeavour to protect and grow your capital.